Introduction to Recognition of Fees under FAS91

FASB refers to the Financial Accounting Standards Board whose critical task is the setting of account standards in the world’s most dynamic economy, that is, the United States of America (USA).

The FASB derives its authority to set accounting standards from the US Securities and Exchange Commission (SEC). The SEC and the American Institute of Certified Public Accountants (AICPA) officially recognise the standards issued by the FASB as authoritative. Investors, lenders and other users of financial information rely on financial reporting based on the U.S. GAAP to decide on how to allocate their capital and help financial markets operate as efficiently as possible.

The Statement of Financial Accounting Standards No.91 (FAS91) establishes the accounting for non-refundable fees and costs associated with lending or committing to lend at amortised cost.

According to the FAS91 requirement, non-refundable fees must be deferred and recognised over the life of the loan as an adjustment of yield, or an Effective Interest Rate (EIR), based on the contractual term of the loan. Loan fees and loan costs are offset against each other and the net amount is deferred and amortised. Thus, it is imperative for banks to determine the cost and fees that are non-refundable relating to a loan, and to amortise them till the maturity of the loan.

The non-refundable fees or associated costs with lending are mostly the loan fees and direct loan origination costs.

Loan fees fall under two categories:

- Origination fees

- Commitment fees

Though the fees are different with minor exceptions, they are treated the same by FAS91, as both the fees are amortised over the term of the loan.

Direct loan origination costs are costs that are directly incurred by the lender for the loan.

FAS 91 Solution for Banks

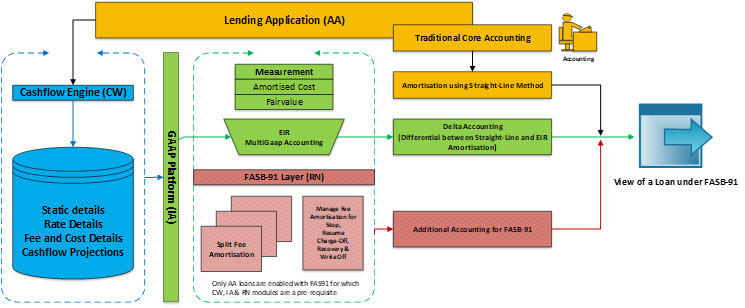

The lending application manages contracts throughout the lifetime of the contract, where users capture the loan arrangement contract with basic details such as loan amount, interest rate, contract term and payment schedule and passes the cash flow projections along with static details, rate details, fees and cost details to the cash flow engine, which is stored in cash flow record.

The IA GAAP platform provides the framework using the following calculations:

- Applying the XIRR formula to calculate the EIR using the projected cash flows along with the dates.

- When future cash flows are discounted using the EIR, the Net Present Value (NPV) of the contractual cash flows of the contract is calculated.

- When future cash flows are discounted using the Market Rate, the Net Present Value of the contract at market rate is calculated.

- Raising multi-GAAP accounting adjustments.

Under the traditional accounting principles, the lending application uses the transactional interest rate for interest recognition and fee/cost amortisation are allowed using the straight-line amortisation method.

The accounting framework allows to raise the accounting movements for the delta between contract balances and the calculated value using the NPV method and is termed as Delta Accounting and is a consolidated delta.

Under FAS91, the accounting of non-refundable fees or cost are amortised using the EIR.

- Temenos Transact supports the FAS91 regulation with the RN module built on top of the GAAP platform.

- The FAS91 layer splits the consolidated delta amount into fees and cost on a pro-rata basis by arriving at a split percentage when loans are in performing status.

- It also supports the managing of fee and cost amortisation during various events on a loan such as:

- Performing loan moving to non-performing status and resuming back to performing status

- Charge-off in case of non-performing loan

- Recovery on charged off loans

- Write offs in case of non-performing loans

AA loans are enabled with FAS91 accounting for which the Cash Flow Generation (CW), IAS39 (IA) & Recognition of Fees (RN) modules are a pre-requisite.

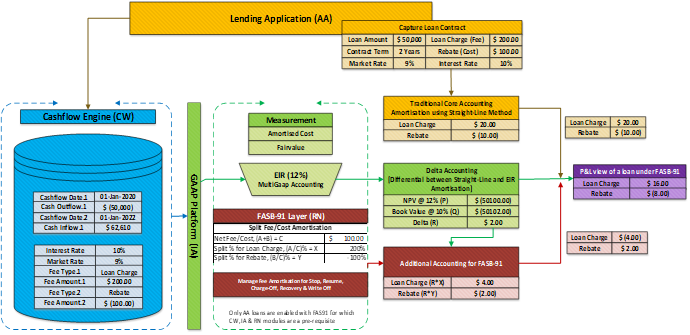

The core accounting under the straight-line method, the delta difference under EIR along with the additional accounting under FAS91 collectively shows the GL view of a loan based on the example below:

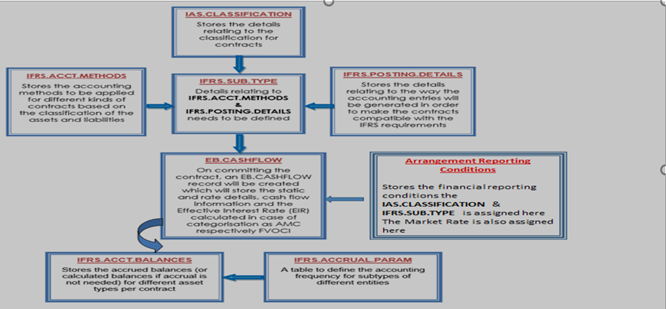

Product Configuration

The parameter configuration required under the accounting framework for the classification and measurement of financial assets are as below:

The following tables are to be configured along with the module configuration under IA:

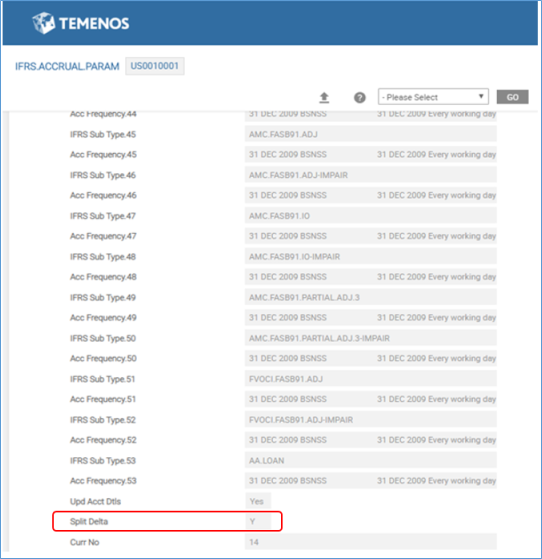

- Set the Split Delta field to Y in the IFRS.ACCURAL.PARAM application.

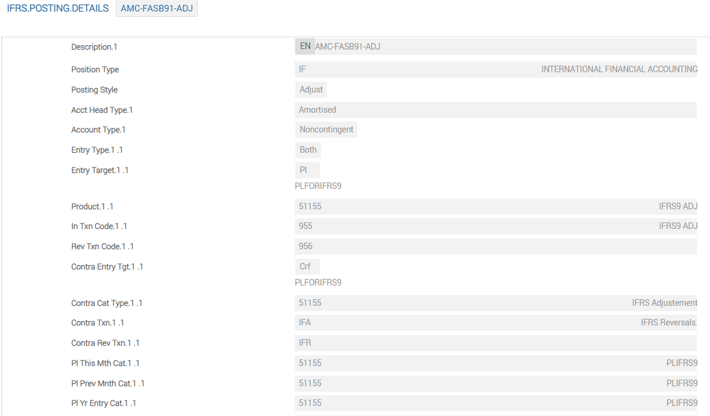

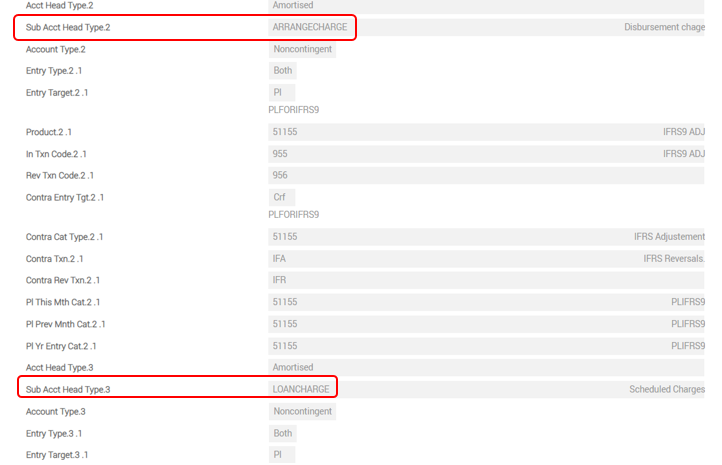

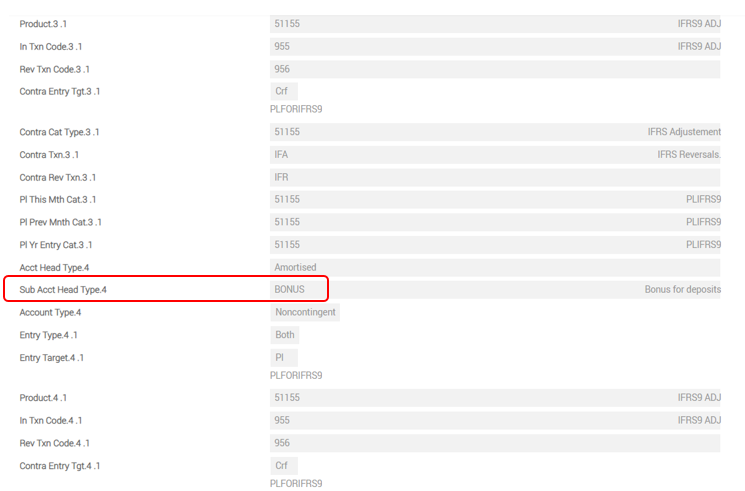

- Define the non-refundable fee and cost in the Sub Acct Head Type field as Amortised in the IFRS.POSTING.DETAILS application.

In this topic